Know

Here’s how Tampa-St. Pete community banks did in Q3

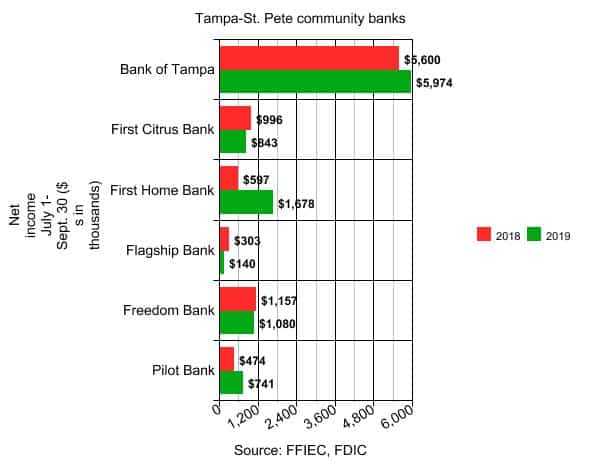

Most locally based community banks are on track to have a more profitable year in 2019 than in 2018.

Net income through the first nine months of 2019 was up at five of the six community banks headquartered in the Tampa-St. Petersburg-Clearwater metro area and with a presence in Pinellas County.

Flagship Bank, based in Clearwater, was the only local bank to see profit fall in the first three quarters of 2019. Flagship was acquired by West Florida Bank Corp. in late October. The new ownership group is made up of veteran bankers from the Tampa-St. Pete area, and raised more than $33 million from 250 local shareholders for the deal, said Bob McGivney, vice chairman and CEO. “We have retained 22 of the 26 Flagship staff members in addition to our plans to expand,” McGivney said.

Local banks’ profits for the third quarter of 2019, the three months ended Sept. 30, were mixed.

First Citrus Bank, headquartered in Tampa, said a 15 percent drop in Q3 earnings was due to increased personnel costs and expansion activities in the Pinellas County market. The bank expects to open its first branch in more than a decade in downtown St. Petersburg in early 2020.

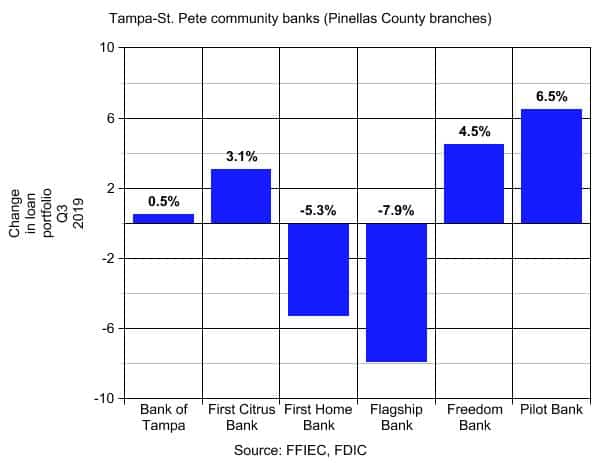

Community banks are a key source of credit for small to mid-size companies in the area. Changes in community banks’ loan portfolios can be a proxy for how eager businesses are to expand, hire and make big purchases.

Most of the community banks grew their loan portfolios in Q3.

Among the local banks, Flagship had the biggest decline in its loan portfolio in the three months ended Sept. 30.

That’s normal for a bank prior to acquisition, McGivney said.

The loan portfolio also shrunk during Q3 2019 at First Home Bank in St. Petersburg. The bank has a fluid balance sheet, because it has large residential mortgage and Small Business Administration lending operations, both of which sell loans into the secondary market, said Tony Leo, CEO. That means the loan balance can vary at any given point in time based on loans held for sale.

The bank sold several SBA loans just before the quarter closed, he said.

“If you look at it over a longer number of quarters you’ll see a truer picture and a more discernable trend. Within any given quarter it will vary fairly substantially. We generate a significant amount of fluid assets, so what’s on the balance sheet at any given time may fluctuate, based on the timing of loan sales,” Leo said.

“If you look at it over a longer number of quarters you’ll see a truer picture and a more discernable trend. Within any given quarter it will vary fairly substantially. We generate a significant amount of fluid assets, so what’s on the balance sheet at any given time may fluctuate, based on the timing of loan sales,” Leo said.

First Citrus Bank has made over $1 billion in loans over the past two decades, Jack Barrett, president and CEO, said at the bank’s recent 20th anniversary celebration.

The bank has grown from $22 million in assets in its first year to $416 million in assets as of Sept. 30.

First Citrus also has one of the highest loan-to-deposit ratios among local banks. The loan-to-deposit ratio indicates how much of the deposits that are taken in by banks are lent out to customers. A low ratio indicates a bank has more deposits it can turn into money-making loans.

Raymond James Bank, part of St. Petersburg-based Raymond James Financial (NYSE: RJF), reported pre-tax net income of $131 million for the three months ended Sept. 30. That was up 1 percent from the prior quarter, but down 5 percent from a year earlier. Raymond James Bank’s loan portfolio grew 1 percent during Q3, helped by the growth of residential mortgage loans and securities-based loans to the company’s Private Client Group clients, a news release said.