Know

St. Pete 10 years after the recession: Fewer banks, tougher rules and plenty of business to go around

Ten years ago, Pinellas County banks were floundering.

The 10 community banks headquartered in Pinellas County with less than $1 billion in assets had a combined net loss of $8.4 million in 2008, as unemployment soared, real estate values plummeted and loans soured.

It’s a much different picture today. There are only three Pinellas-based banks with less than $1 billion in assets currently, but they’ve posted a combined profit of $6.8 million in just the first nine months of 2018. Loan portfolios are growing and balance sheets are relatively clean, with few troubled loans.

Community banks are a key source of credit for small to mid-size companies in the area, so increased loan portfolios are an indication that local businesses are borrowing more money to grow their operations, buy real estate or equipment, and hire more workers.

Cathy Swanson, CEO, Freedom Bank

“There was a period of time when it was more difficult to get credit. Everyone was gun-shy after the recession and rightly so until the market began to stabilize,” said Cathy Swanson, CEO of Freedom Bank, the only remaining community bank headquartered in St. Petersburg.

Businesses held on to their cash during the recession, and while some are still hesitant to borrow, many other companies are in expansion mode, so loan demand is picking up. And, despite tougher regulations and tighter underwriting criteria, banks are lending again.

“I think that in the last 12 to 18 months, maybe 24 months, credit has loosened up somewhat,” Swanson said. “There’s a lot of liquidity in the market, and I think banks are seeing that as an opportunity to be a little bit less conservative and get good assets on the books.”

Commercial banking depends largely on building strong relationships between borrowers and lenders, said Leslie Bridges, a St. Petersburg-based first vice president and loan officer at Valley. “Do a good job, get your name out there and you get a lot of incoming requests. There’s a ton of business for everybody.”

Shrinking numbers

The number of banks has shrunk dramatically nationally and locally since the Great Recession.

There were 307 banks headquartered in Florida at the end of 2008, compared to 118 now.

Seventy-two Florida banks failed during the economic downturn, including Old Harbor Bank in Clearwater. Others were purchased by mid-sized banks from out of state that wanted to capitalize on Florida’s growing population, in order to beef up their deposit base and make more loans. Among the bigger banks that were acquired were USAmeriBank, bought by Valley National Bancorp (NASDAQ: VLY) earlier this year, and C1 Bank, bought by Bank of the Ozarks, now Bank OZK (NASDAQ: OZK) in 2016.

View Pinellas County banks in a full screen map

Fewer banks can mean less options for businesses seeking loans, but for Freedom Bank, it’s meant more opportunity, Swanson said.

“There are still people in our market, small businesses and professionals, who want to do business with a local community bank. As those numbers dwindle, it allows us to become more prominent in the community and we can take advantage of that,” she said.

David Feaster, Florida market president, Republic Bank

Consolidation has slowed recently, as the price of the remaining banks is a much higher multiple of book value, said David Feaster, Florida market president for Republic Bank, a Louisville, Kentucky-based bank that bought Cornerstone Community Bank in St. Petersburg in 2016.

There’s been only a handful of new banks nationwide, including Gulfside Bank in Sarasota, which opened on Nov. 13.

“I’m still surprised there aren’t more de novo banks,” Feaster said. “I started a bank in 1999, and I’ll bet there were 40 in Florida. From 1998 to 2005, my gosh, the number of banks that opened. Now the capital requirements are stricter and [with] the amount of compliance involved, you are seeing fewer than you did.”

Dodd-Frank, the 2010 law that imposed new banking rules and created the Consumer Financial Protection Bureau, has had a financial impact on the banking industry.

“Banking needs to be highly regulated. However, after most crises the government many times overreacts and the level of compliance has become burdensome. Many little banks literally couldn’t comply, because of the expense involved — hundreds of millions of dollars,” Feaster said.

Industry standards changed as well.

“Underwriting is much better. I’m a better banker today than I was in 2008,” Feaster said. “It used to be that many bankers were just collateral bankers, ‘give me 80 percent loan-to-value, and I’m fine on a piece of real estate.’ Today, we ask about the source of repayment, the real cash flow and real equity in the project.”

Using real estate as collateral was a common practice when Bridges entered the banking industry in 2008 at the former Bank of St. Petersburg.

“They used to say in loan committees, if you have dirt you can’t get hurt,” said Bridges.

Leslie Bridges, first vice president, loan officer, Valley

That practice backfired when real estate values dropped dramatically during the downturn.

She joined USAmeriBank in 2011 and stayed on after the bank was acquired by Valley, where the practice is to match the need for the loan with the collateral.

“If someone needs a short-term loan for working capital, you don’t necessarily secure that with real estate, ” she said. “In certain instances, you have to do that if the deal isn’t strong enough. But if it’s strong enough, you are helping the borrower. They’re in a better spot when they want to expand or improve their building.”

Technology’s impact

The banking industry’s use of technology has exploded since 2008.

Large banks such as JPMorgan Chase & Co. (NYSE: JPM) have poured billions of dollars into new products for digital banking and cybersecurity, Institutional Investor reported. JPMorgan will open a financial technology campus next year in Silicon Valley, according to CNBC.

Smaller banks can take advantage of the “bleeding-edge” technology developed by the bigger institutions.

“There’s just a handful of core banking systems and core providers and they are duplicating their efforts over and over for each bank,” Swanson said. “We have access to all that technology. It’s just a matter of deciding to invest in it.”

Technology such as remote deposit capture that allows checks to be scanned and deposited online, along with mobile banking, means there are fewer branch offices. Customers rarely go into a bank office now, Feaster said.

There were 341 bank offices with a combined $25.9 billion in deposits in Pinellas County on June 30, 2008, compared to 286 bank offices with a combined $44.6 billion in deposits on the same day 10 years later.

“The metric to justify a branch used to be $15 million to $20 million in deposits. Today, a branch needs to be $40 million to $50 million,” Feaster said. “It’s called a non-earning asset and it’s expensive.”

While some former bank branches are being turned into other kinds of office space or restaurants, “real estate investors who own those buildings are challenged with finding viable tenants or buyers for those locations,” Swanson said.

She sees a strong economy ahead for the next 12 to 18 months.

Feaster doesn’t anticipate a repeat of 2008, although he’s keeping a close eye on home and apartment construction for signs of over-saturation that would signal trouble.

“The antenna is up. That doesn’t mean there’s an issue … but bankers are by nature conservative and if something grows too fast, that scares us,” he said.

Closer look: Pinellas County community banks

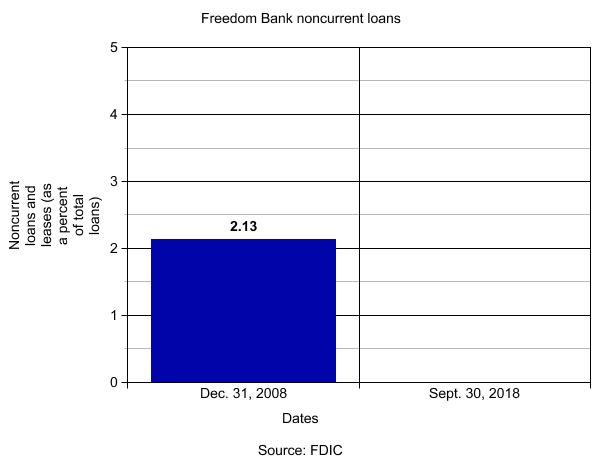

Freedom Bank, St. Petersburg

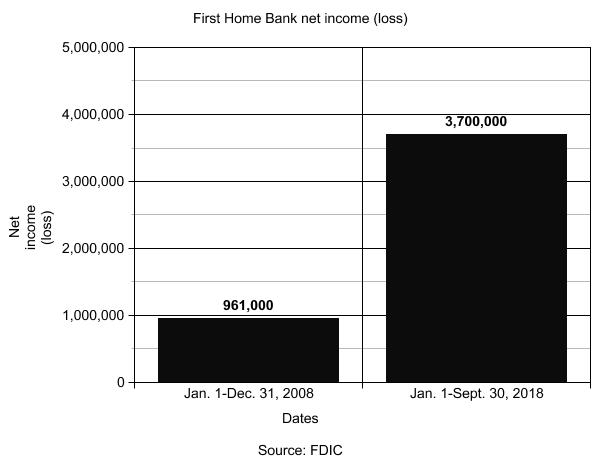

First Home Bank, Seminole

Flagship Community Bank, Clearwater

Mike Manning

December 6, 2018at5:15 pm

St. Petersburg is chugging along, but I wonder what happens when middle and lower classes get completely squeezed out. Housing and bank loans are increasingly difficult to obtain. Community banking mostly means credit unions to them,and interest rates are going up everywhere.