Know

What will Milton cost insurers and homeowners?

Moody’s Analytics believes Hurricane Milton is among the costliest hurricanes to strike the U.S., with estimated insurance losses between $30 billion and $50 billion.

Morningstar DBRS analysts believe that number is in the “upper half” of its initial $30 billion to $60 billion forecast. The global credit ratings agency predicts Milton will cost the National Flood Insurance Program (NFIP) $10 billion.

“Milton could also cause close to $100 billion in economic damage, which includes insured as well as uninsured losses,” Morningstar wrote in an Oct. 14 study. “Indeed, the hurricane heavily affected the areas with high reconstruction costs and struck in close proximity to the Tampa metropolitan area – a major economic hub in Florida.”

St. Petersburg officials hope insurance will cover Tropicana Field’s damages. Photo by Mark Parker.

The report’s researchers added that the region, also still reeling from Hurricane Helene, is among the nation’s top 25 economic producers by gross domestic product. The estimated losses place Milton’s costs on par with Hurricane Ian in 2022.

Moody’s believes insured losses for Hurricane Helene are between $8 billion and $14 billion. Mohsen Rahnama, chief risk modeling officer, noted the back-to-back storms present an additional challenge.

Preliminary reports indicated several uninsured or underinsured structures flooded by Helene incurred additional impacts from Milton’s typically covered gusts and wind-driven rain. Rahnama said that could lead to “coverage leakage,” or insurers paying for non-covered costs.

“If a claim was opened after Helene, and if there is additional damage in Hurricane Milton, it will likely result in a single payout,” Rahnama explained. “But there will be questions on which event the payout is assigned to – and the resulting impact on potential reinsurance recoveries.”

The Moody’s report also noted that most homeowner policies in Florida have an annual hurricane deductible. Insurers will likely face higher losses for damage caused by Milton to structures with deductibles exhausted after Helene.

Citizens Property Insurance, the state-backed insurer of last resort, has struggled to stay solvent for the past several years as many large national insurers have vacated Florida’s residential market. “As such, Citizens will bear a significant portion of the anticipated losses,” states Morningstar’s report.

However, the firm’s researchers believe Citizens will maintain its “financial strength” as a government-supported entity that can levy assessments on existing policyholders. They also expect large national insurers that dominate local markets, like State Farm, to absorb extensive losses.

Morningstar wrote that small to mid-size private insurers will face “significant earning pressure.” Researchers predict that reinsurance prices will likely increase, “reversing the signs of price stabilization observed during the 2024 mid-year renewal season.”

“Historically, large increases in reinsurance prices have happened after severe insured losses,” concluded Morningstar. “Unfortunately, if our forecasts materialize, this is bad news for households and businesses relying on property insurance for protection from severe weather as those prices have nowhere to go but up.”

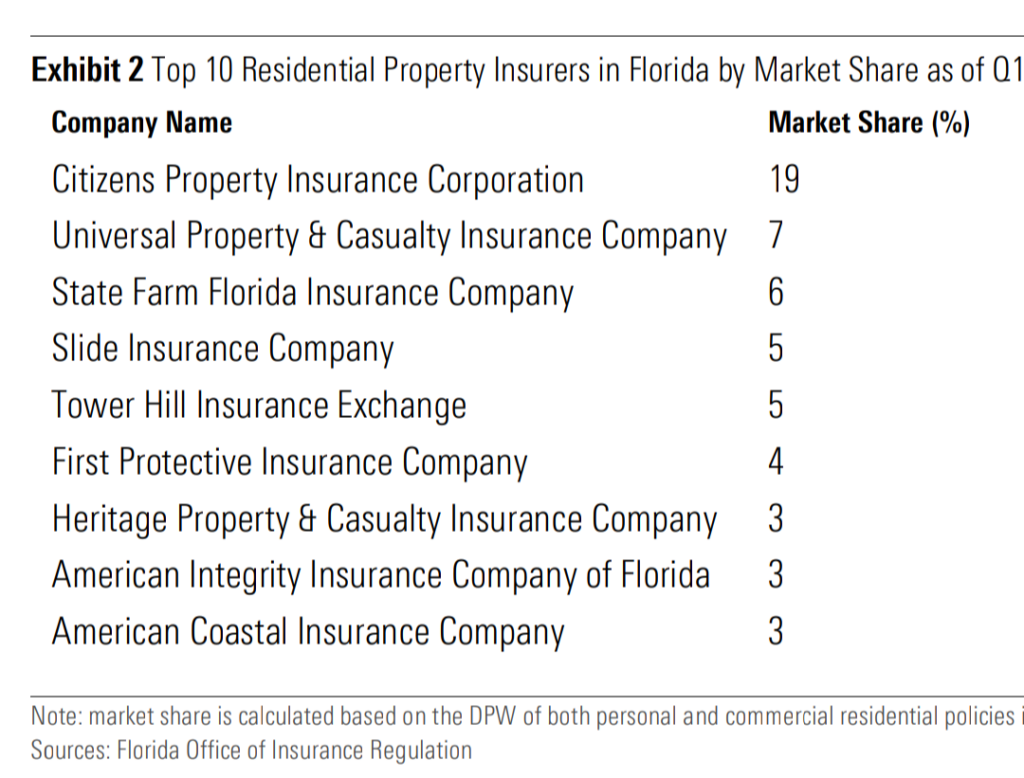

A list of the top residential property insurers in Florida according to market share percentage. Image: Moody’s Analytics.

Robert Guinn, a partner at Tampa-based Cole, Scott & Kisssane, the state’s largest civil litigation firm, said residents affected by Helene and Milton might lack vital coverage. The storm claim-focused attorney told the Catalyst that consumers often forego wind protection yet still attempt to recoup hurricane-related losses.

Guinn expects rates to continue rising after an extraordinary hurricane season. He also believes recent losses will mitigate the state legislature’s recent attempts to limit insurance company exposures “in an effort to drive down those costs.”

“I don’t know if there’s anything an average consumer can do other than ensure the properties they have are protected and that they are taking care of their properties,” Guinn added. “So, if an event is happening or about to happen, the home is protected. And maybe a claim, frankly, doesn’t need to be made.

“If a home is in properly maintained condition, and it’s able to withstand storms, ultimately, it will result in fewer claims and premium increases for the average consumer.”

Homeowners’ insurance policies do not cover flood damage. In addition, a November 2023 report from the University of South Florida St. Petersburg’s Customer Experience Lab found that over 73% of homeowners falsely believe they have flood insurance.

St. Petersburg-based Neptune Flood recently announced that just 12% of 8.97 million properties in Florida have flood insurance. CEO Trevor Burgess has repeatedly warned of a “massive disconnect.”

He previously noted that about 25% of Pinellas County homeowners have flood insurance. “Hello, we’re a peninsula on a peninsula,” he said. “Every single house should have flood insurance.”